I think it's safe to say that we're ALL ready to leave 2020 behind.

One thing I'm walking into 2021 with is a set of new, improved financial habits. There's nothing like a new year with a new slate to make you feel motivated to put your best (financial) foot forward. Here are some money tips that'll help:

1.Get as specific as possible when it comes to creating your money goals.

2.Create a simple budget to avoid overspending.

3.Check your accounts regularly to make sure there aren't any unfamiliar charges eating up your money.

4.Set designated "no-spend" days so you can curb your spending in small ways.

5.Automate your bills so you never miss a monthly due date (and get charged those money-munching late fees).

6.Pay a little more than just the minimum payment on at least one of your debts.

7.Start building an emergency fund — even if you just start by setting aside $100 a month for unexpected expenses.

8.Learn as much as you can about saving for retirement.

9.Invest in yourself.

10.Think about the items you'd like to spend more on — and budget for them.

11.Keep your bank info in a safe place so you won't have to stress about forgetting your credentials.

12.Take a long, hard look at all the services you're subscribed to and cancel the ones you don't need anymore.

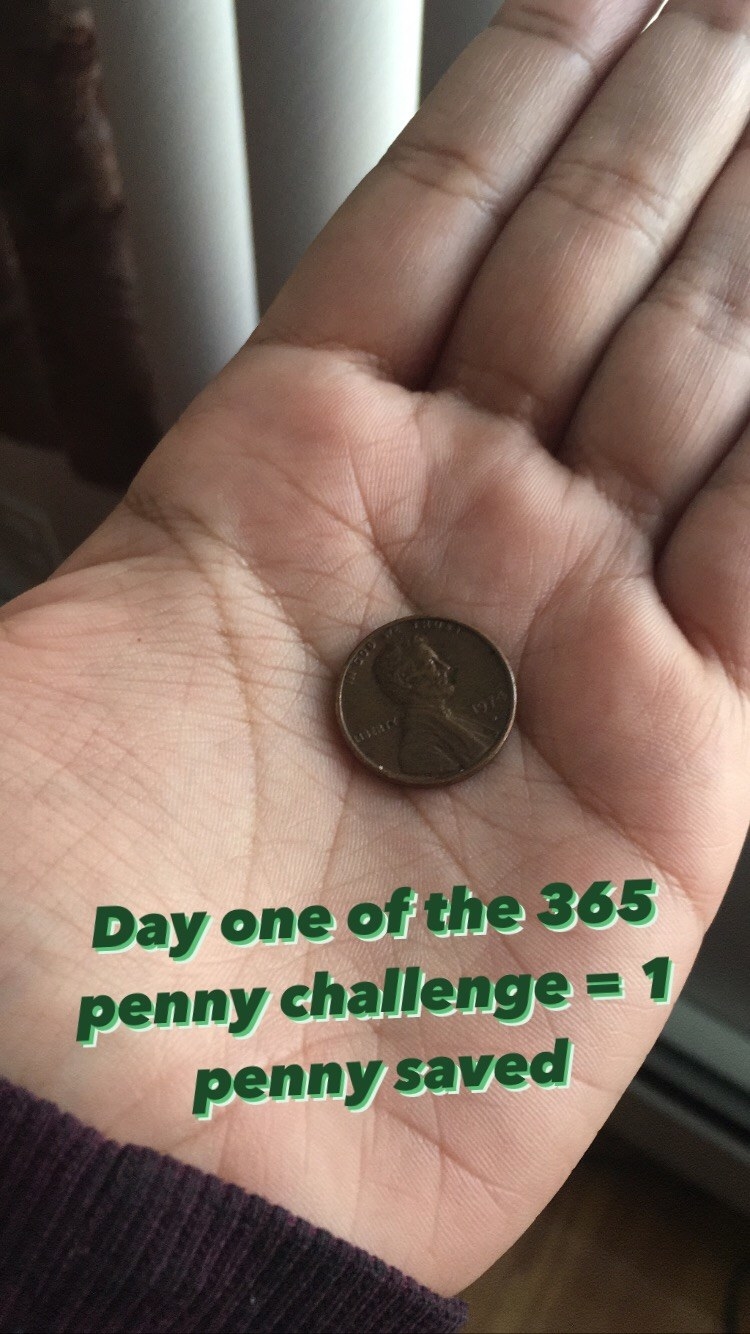

13.Come up with creative ways to save money to make the process feel less daunting.

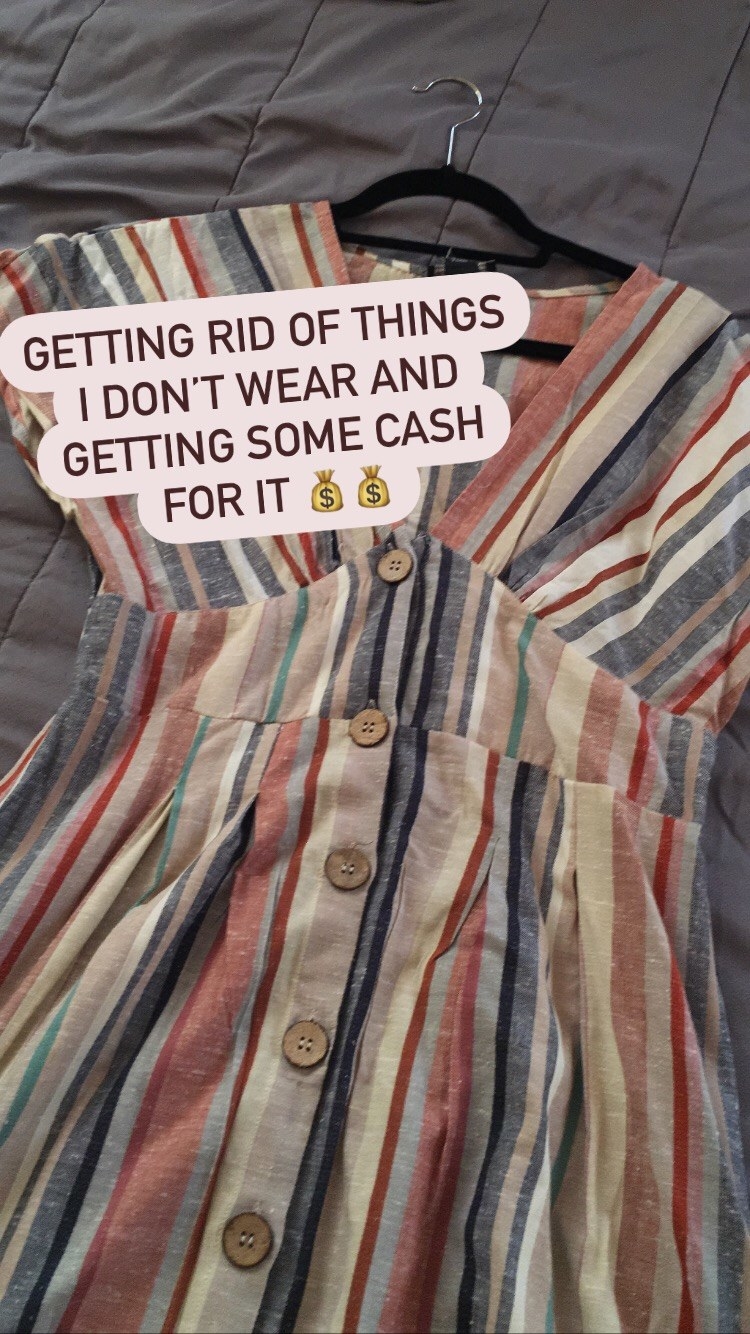

14.Sell unwanted items so you can declutter your life AND make some extra cash for savings or new purchases.

15.Dump the pressure of keeping up with the Joneses.

16.Work up the courage to have some of the difficult money conversations (that you usually sweep under the rug).

17.Be open to learning more about managing your money.

What are your money resolutions for the new year? Share 'em below, and you could be featured in an upcoming post.

If this sounds like music to your ears (and bank account), check out more of our personal finance posts.

{kind=link}