{kind=link}

Here’s a scary stat: According to the Federal Reserve, 40% of Americans don’t have a spare $400 to cover an emergency cost. That’s pretty demoralizing, considering the term “emergency expense” casts a wide net of situations.

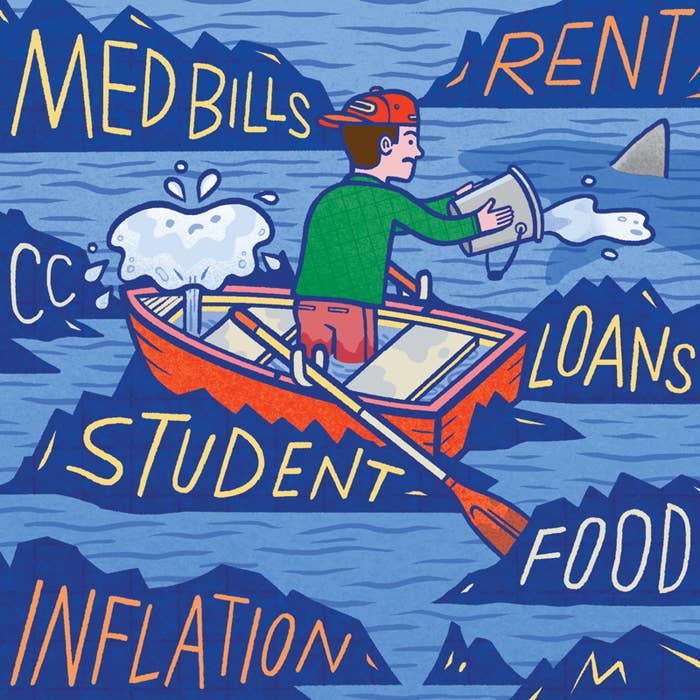

Why People Aren’t Saving

How to Start Saving

Yes, the idea of saving thousands of dollars might feel unattainable — but you can start. Below are the action steps you can put in place today to help you better position yourself financially.

1. Put Other Financial Game Plans on Hold

2. Pay Yourself First

3. Put Money in a Separate Bank

4. Earn That Interest

5. Set Multiple Goals