{kind=link}

True story: I'm a first-time pregnant lady and have no idea what I'm doing — especially when it comes to financially preparing for this change.

In an effort to face reality, I chatted with Chantel Bonneau at Northwestern Mutual, who is not only a finance expert but also a mom herself.

1. Bonneau says that before your baby comes (or, better yet, before you start trying), you need to get real about what your life will look like post-baby.

2. Turns out I need to take time NOW to clean up my finances.

3. Bonneau notes that if finances aren't your cup of tea, you can seek out a financial adviser to help you budget and plan for your new addition.

4. I learned that now is also the time to talk about estate planning and beneficiaries.

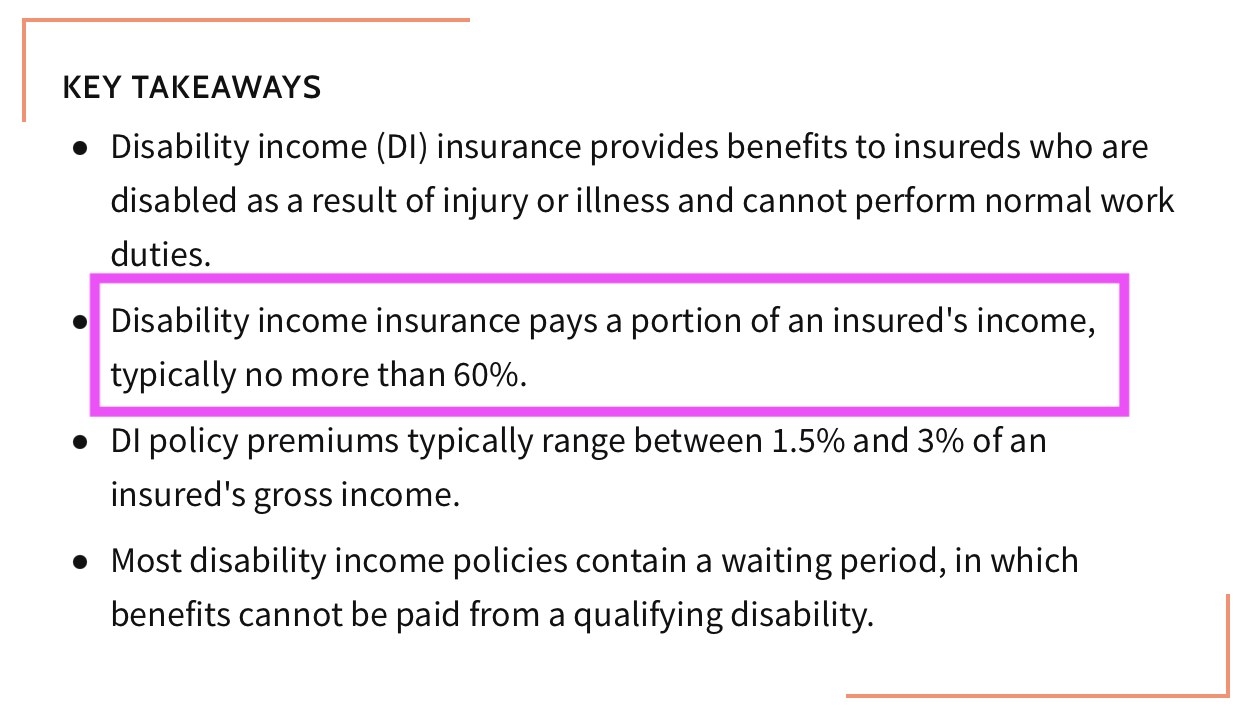

5. If you don't already have it (I don't!), Bonneau says, you should consider buying life and disability insurance.

6. I learned that in addition to looking into the distant future, I need to keep the near future in mind. Most notably, coming up with a plan to pay for the birth.

7. Bonneau says you should also have an idea of how much you can afford to spend on baby stuff, then stay within that budget.

8. And she says to ask your company about parental leave.

9. Keep in mind that one of the biggest costs of having kids is childcare (or quitting your job to provide care).

10. If money is tight, don't stress it. There are always ways you can cut back in other areas to make room for this new cost.

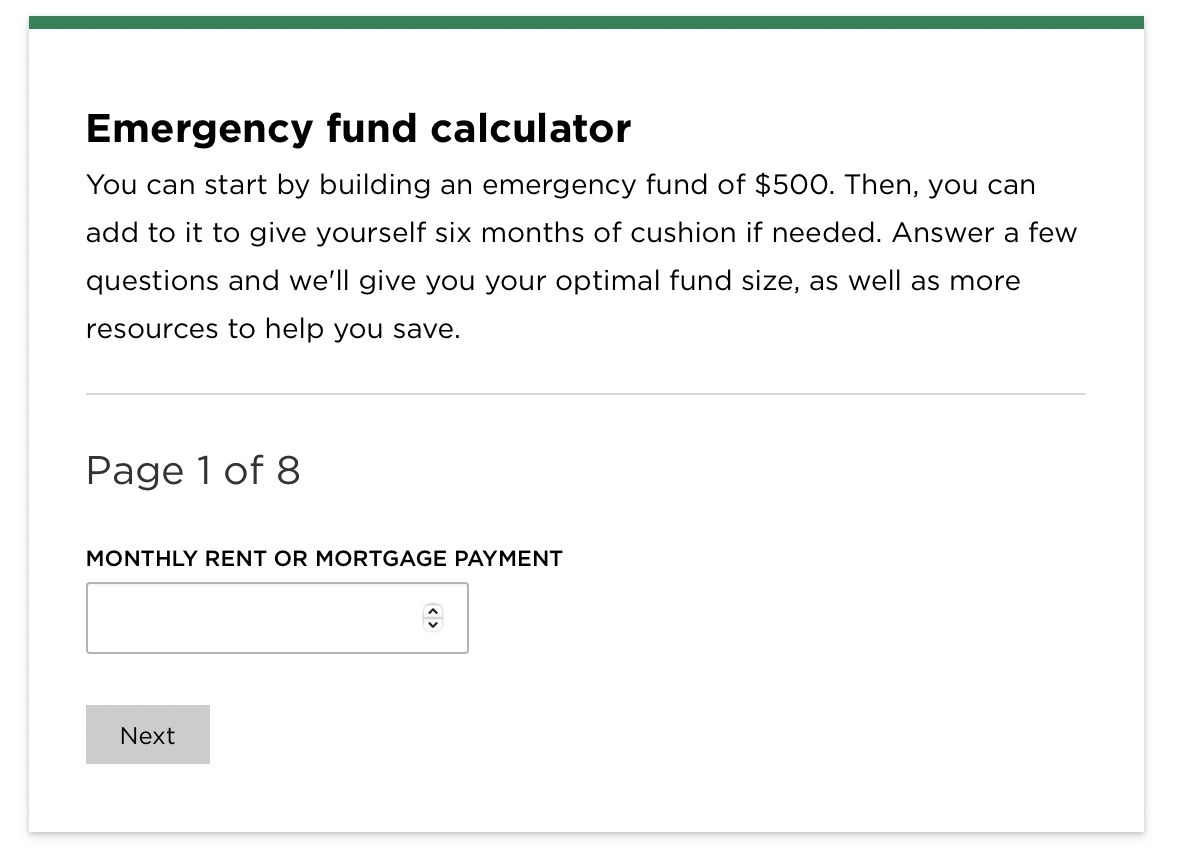

11. Based on the anticipated monthly cost of the new addition, I'll need to reconfigure my emergency fund.

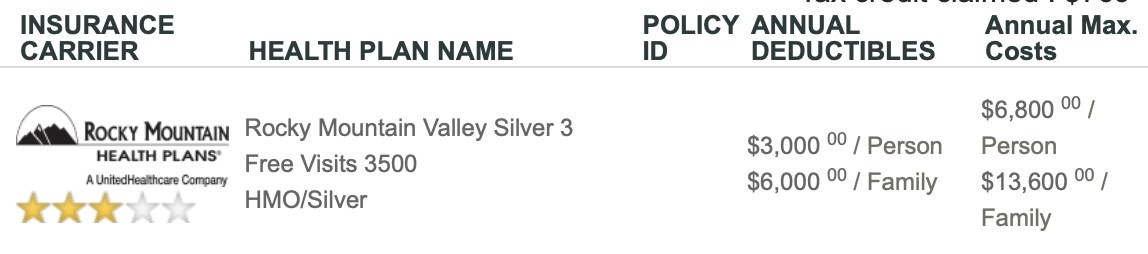

12. And Bonneau reminds new parents that once your babe arrives, you'll need to add them to your health insurance plan.

13. Plus, she says you might also consider buying your new baby life insurance.

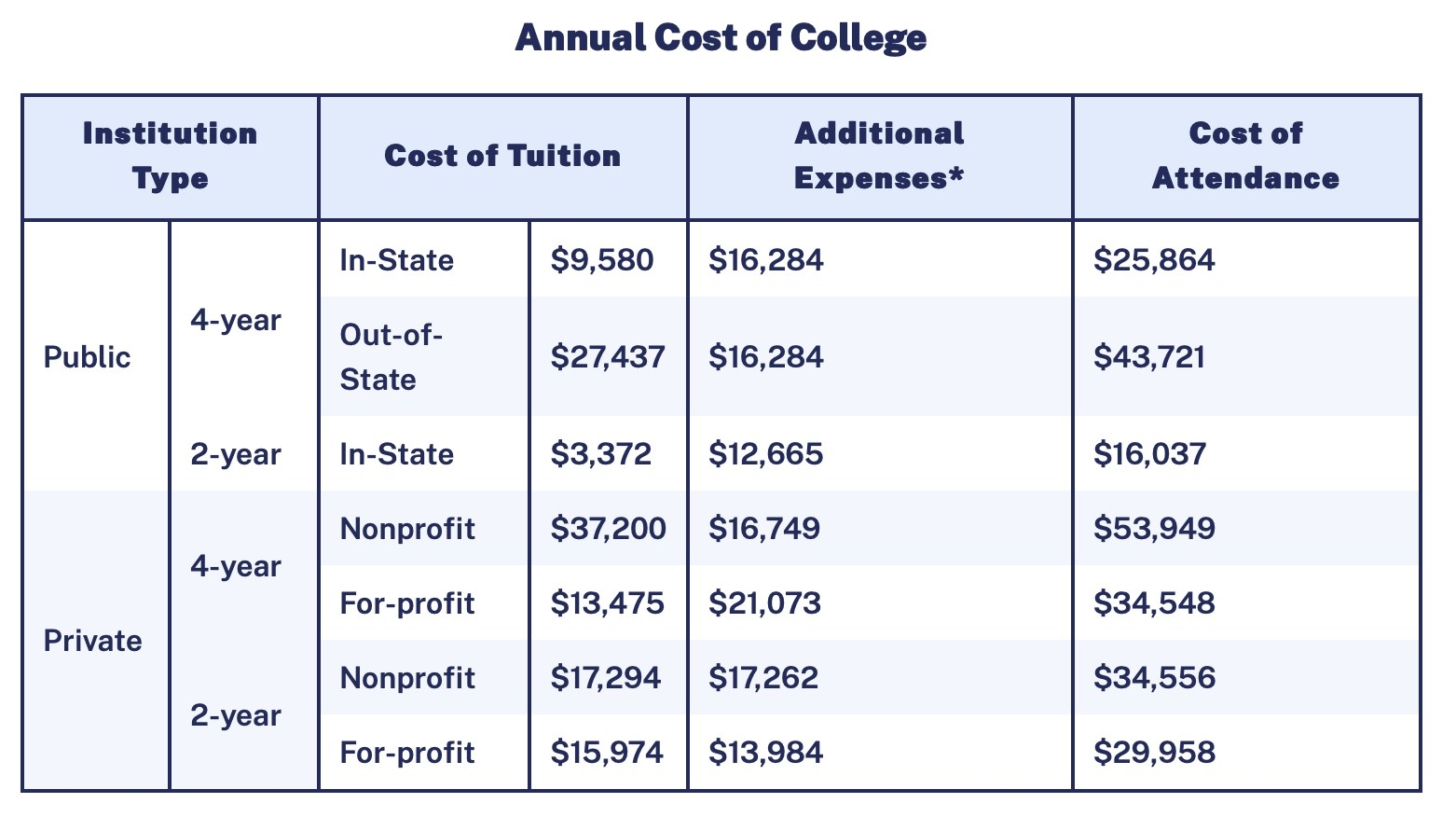

14. And finally, I learned that if there's any money left over, I should consider putting cash aside for my kid's college fund.

Any seasoned parents out there up for sharing their financial tips? Some of us (ahem, me) could use all the help we can get.

And for more money tips and tricks, check out the rest of our personal finance posts.