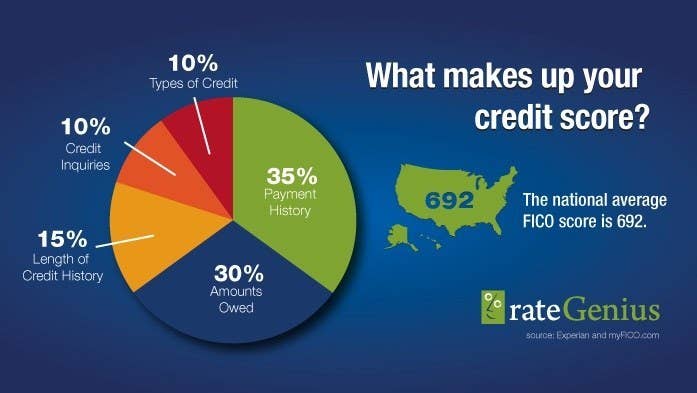

1.

Know how your credit score works.

2.

Start with just one credit card to build your credit.

3.

Always avoid store credit cards.

4.

Want a great chance at your first card? Go to your bank or get a college card.

5.

If you get rejected for a credit card application, you can call a reconsideration line for a second chance.

6.

Still having a hard time getting a credit card? Get a secured credit card.

7.

You can even ask a parent or spouse to get an "authorized" copy of their card to build your score.

8.

If you want more credit cards, wait at least 8 months and then apply.

9.

Hate getting those credit card offers in the mail? You can stop them.

10.

Don't be afraid to ask for a credit card limit increase if you've been good.

11.

Remember! You have the right to three, totally free credit reports a year.

12.

Cool score boosting tip: Pay down your card to a small amount, let your statement come in, then pay it off in full.

13.

Remember that a free credit score is a good estimate of your actual credit score.

14.

Always pay on time, no matter what.

15.

...but if you don't, pay off your debt as fast as you can!

16.

It's actually good to have different kinds of credit/debt for your credit score.

17.

And of course, never spend what you can't pay back.

{kind=link}