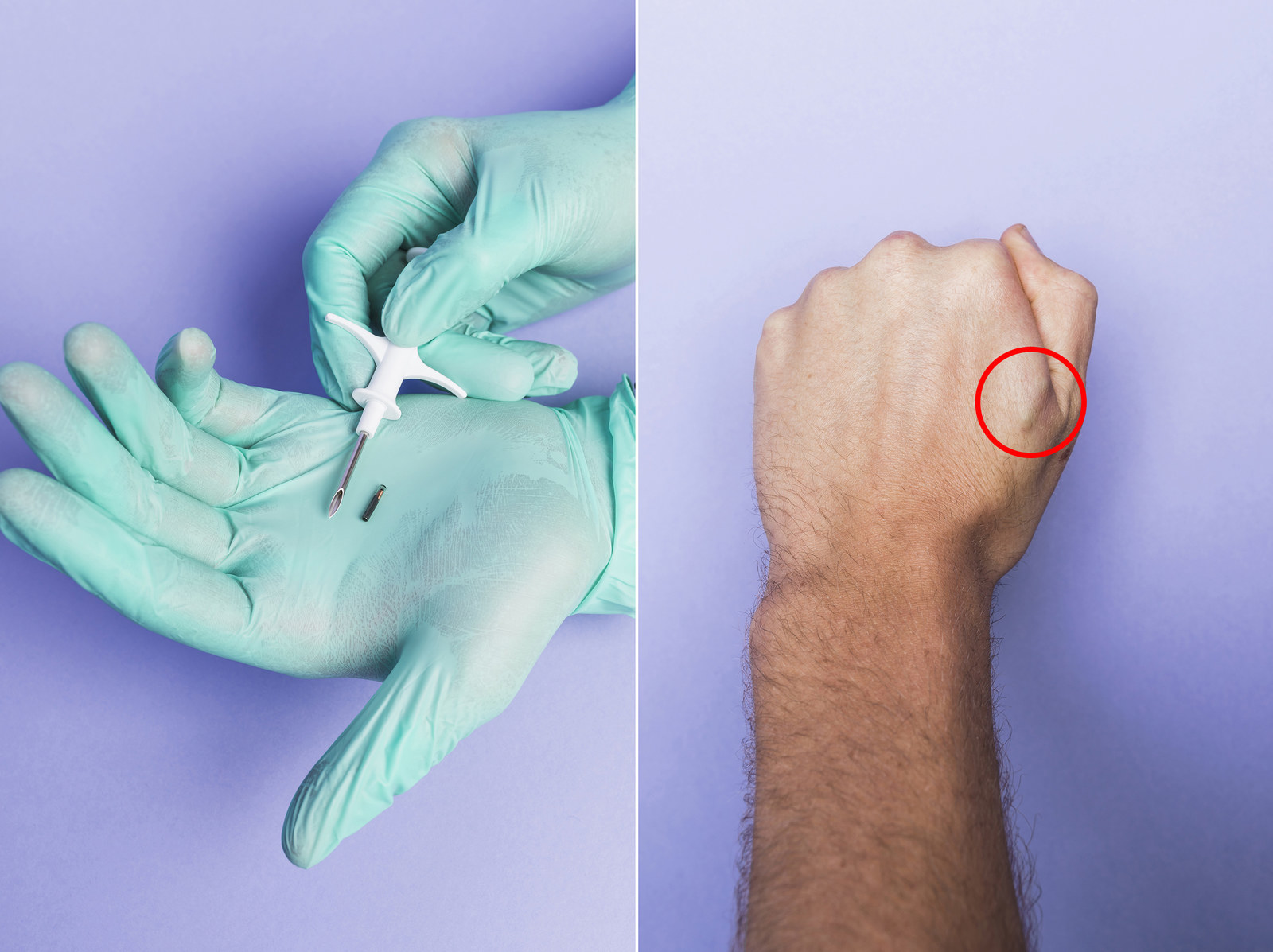

It’s the dead of winter in Stockholm and I’m sitting in a very small room inside the very inaptly named Calm Body Modification clinic. A few feet away sits the syringe that will, soon enough, plunge into the fat between my thumb and forefinger and deposit a glass-encased microchip roughly the size of an engorged grain of rice.

“You freaking out a little?” asks Calm’s proprietor, a heavily tattooed man named Chai, as he runs an alcohol-soaked cotton swab across my hand. “It’s all right. You’re getting a microchip implanted inside your body. It’d be weird if you weren’t freaking out a little bit.” Of Course It Fucking Hurts!, his T-shirt admonishes in bold type.

My choice to get microchipped was not ceremonial. It was neither a transhumanist statement nor the fulfillment of a childhood dream born of afternoons reading science fiction. I was here in Stockholm, a city that’s supposedly left cash behind, to see out the extreme conclusion of a monthlong experiment to live without cash, physical credit cards, and, eventually, later in the month, state-backed currency altogether, in a bid to see for myself what the future of money — as is currently being written by Silicon Valley — might look like.

Some of most powerful corporations in the world — Apple, Facebook, and Google; the Goliaths, the big guys, the companies that make the safest bets and rarely lose — are pouring resources and muscle into the payments industry, historically a complicated, low-margin business. Meanwhile, companies like Uber and Airbnb have been forced to become payments giants themselves, helping to facilitate and process millions of transactions (and millions of dollars) each day. A recent report from the auditor KPMG revealed that global investment in fintech — financial technology, that is — totaled $19.1 billion in 2015, a 106% jump compared to 2014; venture capital investment alone nearly quintupled between 2012 and last year. In 2014, Americans spent more than $3.68 billion using tap-to-pay tech, according to eMarketer. In 2015, that number was $8.71 billion, and in 2019, it’s projected to hit $210.45 billion. As Apple CEO Tim Cook told (warned?) a crowd in the U.K. last November, “Your kids will not know what money is.”

To hear Silicon Valley tell it, the broken-in leather wallet is on life support. I wanted to pull the plug. Which is how, ultimately, I found myself in this sterile Swedish backroom staring down a syringe the size of a pipe cleaner. I was here because I wanted to see the future of money. But really, I just wanted to pay for some shit with a microchip in my hand.

The first thing you’ll notice if you ever decide to surrender your wallet is how damn many apps you’ll need in order to replace it. You’ll need a mobile credit card replacement — Apple Pay or Android Pay — for starters, but you’ll also need person-to-person payment apps like Venmo, PayPal, and Square Cash. Then don’t forget the lesser-knowns: Dwolla, Tilt, Tab, LevelUp, SEQR, Popmoney, P2P Payments, and Flint. Then you might as well embrace the cryptocurrency of the future, bitcoin, by downloading Circle, Breadwallet, Coinbase, Fold, Gliph, Xapo, and Blockchain. You’ll also want to cover your bases with individual retailer payment apps like Starbucks, Walmart, USPS Mobile, Exxon Speedpass, and Shell Motorist, to name but a few. Plus public and regular transit apps — Septa in Philadelphia, NJ Transit in New Jersey, Zipcar, Uber, Lyft. And because you have to eat and drink, Seamless, Drizly, Foodler, Saucey, Waitress, Munchery, and Sprig. The future is fractured.

This isn’t lost on Bryan Yeager, a senior analyst who covers payments for eMarketer. “This kind of piecemeal fragmentation is probably one of the biggest inhibitors out there,” he said. “I’ll be honest: It’s very confusing, not just to me, but to most customers. And it really erodes the value proposition that mobile payments are simpler.”

On a frigid January afternoon in Midtown Manhattan, just hours into my experiment, I found myself at 2 Bros., a red-tiled, fluorescent-lit pizza shop that operates with an aversion to frills. As I made my way past a row of stainless steel ovens, I watched the patrons in front of me grab their glistening slices while wordlessly forking over mangled bills, as has been our country’s custom for a century and a half. When my turn came to order, I croaked what was already my least-favorite phrase: "Do you, um, take Apple Pay?" The man behind the counter blinked four times before (wisely) declaring me a lost cause and moving to the next person in line.

This kind of bewildered rejection was fairly common. A change may be coming for money, but not everyone’s on board yet, and Yaeger's entirely correct that the "simple" value proposition hasn't entirely come to pass. Paying with the wave of a phone, I found, pushes you toward extremes; to submit to the will of one of the major mobile wallets is to choose between big-box retailers and chain restaurants and small, niche luxury stores. The only business in my Brooklyn neighborhood that took Apple Pay or Android Pay was a cafe where a large iced coffee runs upwards of $5; globally, most of the businesses that have signed on as Apple Pay partners are large national chains like Jamba Juice, Pep Boys, Best Buy, and Macy’s.

Partially for this reason, the primary way most Americans are currently experiencing the great fintech boom isn’t through Apple or Android Pay at all, but through proprietary payment apps from chains such as Target, Walmart, and Starbucks — as of last October, an astonishing 1 in 5 of all Starbucks transactions in the U.S. were done through the company’s mobile app. It wouldn’t be all that hard to live a fully functional — if possibly boring — cash-free consumer life by tapping and swiping the proprietary apps of our nation’s biggest stores.

If that doesn’t feel revolutionary or particularly futuristic, it’s because it’s not really meant to. But the future of mobile retail is assuredly dystopian. Just ask Andy O’Dell, who works for Clutch, a marketing company that helps with consumer loyalty programs and deals with these kinds of mobile purchasing apps. “Apple Pay and the Starbucks payment app have nothing to do with actual payments,” he told me. “The power of payments and the future of these programs is in the data they generate.”

"The power of payments is in the data they generate.”

Imagine this future: Every day you go to Starbucks before work because it’s right near your house. You use the app, and to ensure your reliable patronage, Starbucks coughs up a loyalty reward, giving you a free cup of coffee every 15 visits. Great deal, you say! O’Dell disagrees. According to him, Starbucks is just hurting its margins by giving you something you’d already be buying. The real trick, he argued, is changing your behavior. He offers a new scenario where this time, instead of a free coffee every 15 visits, you get a free danish — which you try and then realize it goes great with coffee. So you start buying a danish once a week, then maybe twice a week, until it starts to feel like it was your idea all along.

In that case, O’Dell said, Starbucks has "changed my behavior and captured more share of my wallet, and they've also given me more of what I want."

"That's terrifying," I told him.

"But that’s the brave new world, man," he shot back. "Moving payments from plastic swipes to digital taps is going to change how companies influence your behavior. That's what you're asking, right? Well, that's how we're doing it."

In this sense, the payments rush is, in no small part, a data rush. Creating a wallet that’s just a digital version of the one you keep in your pocket is not the endgame. But figuring out where you shop, when you shop, and exactly what products you have an affinity for, and then bundling all that information in digestible chunks to inform the marketers of the world? Being able to, as O’Dell puts it, “drive you to the outcome they want you to have like a rat in a maze by understanding, down to your personality, who you are”? That’s disruption worth investing in.

For all its complexity and bureaucracy and importance, money, at its core, is really just information. When FDR weaned the United States off the gold standard in 1933, cash, no longer backed by physical gold, became an abstraction. Today, that abstraction is pushed to new extremes: Not only does 92% of the money in the world exist as a series of ones and zeroes, but now it’s being transferred from place to place by any number of digital intermediaries looking to take a cut.

That process is complicated, but the key issue is trust. Money, argues David Wolman in The End of Money, is not much more than “a belief in a shared purpose, or at least a shared hallucination.” This faith in the “particular religion” of cash has been at the center of standardized currencies since Kublai Khan, and the loss of that faith has been associated with every major economic catastrophe in history. But trust — especially when it comes to new forms of currency — takes time to build.

The first two weeks of my experiment, most people balked when I offered an alternative means of payment. “I’m a little worried this might not go through in time,” one server at a German beer hall told me when I asked if I could Venmo her for my bill. A waiter at a different establishment scoffed when I tried to pay him or the restaurant via PayPal, suggesting his manager would think he was getting ripped off.

Yaeger sees this as standard for a nascent technology. “I kind of equate now to where things were 10 to 12 years ago with e-commerce,” he told me. “The concept of putting credit cards on a screen was new. Retailers and normal people were concerned about that. So innovative companies like PayPal and Amazon built that trust up over a decade while others slowly moved in.”

There are, of course, legitimate reasons not to trust these new forms of payment. Anyone who’s been mugged or lost a wallet knows cash is far from perfect, but this constellation of new digital payment products introduces a whole new category and scale of ways to get robbed, hacked, scammed, and screwed. Venmo — the social payment service that’s now transferring over $1 billion per month — may, in some ways, be the truest glimpse at a mobile payment future, but it’s not exactly entirely secure. Smartphones can be as easily lost and stolen as wallets, but they’re also eminently breakable, orders of magnitude more expensive, and obsolete after two or three years. And the payment-apps landscape is still such that living cashlessly in 2016 means entering your credit card information or routing number into dozens of stand-alone apps, some of which look as if they’ve been built overnight by a high school computer science class.

All this risk and all this friction, in the service of...what, exactly? “Plastic works really well,” Randy Reddig, an entrepreneur who was a part of Square’s founding team, told me, taking a shot at what he called “mobile wallet hysteria.” “I have a wallet right now in my pocket, and it’s great. It can feel like this is something that nobody is asking for. It’s solutioneering: Take something that exists just fine in the meatspace world and make it digital and somehow we’re all supposed to believe it’s better.”

To Reddig, the true future of payments is revealing itself inside many of Silicon Valley’s biggest new companies. Airbnb, he said, has one of the most sophisticated payments infrastructures of any company in the world, handling deposits and disbursements in hundreds of markets, many with different currencies. “All the innovation around payments is a means to an end — table stakes,” he said. “Uber has one of, if not the most used mobile payments methods in the world, and it was absolutely crucial — they had to do it to create the experience and service they wanted. Payment technology created certainty for riders and drivers that they’d get paid — it facilitated trust.”

Much as the true value of a retailer’s mobile payment app is in the metadata it gobbles up, the real power of digital payments lies in the largely invisible infrastructure that undergirds them. Fintech companies like Square aren’t exactly sexy, but they allow small businesses and individual merchants to process transactions without prohibitively expensive equipment or the fees that legacy credit companies charge.

"Millennials don't trust banks, but they trust Apple and Google."

“It’s about financial inclusion and serving real, normal people,” Reddig said. "There is a lot of opportunity to build very profitable businesses that operate better than incumbents in transparency, great design, great user experience. Millennials don't trust banks, but they trust Apple and Google."

This is already happening, just outside the U.S. If fintech’s true believers think it’ll fundamentally change the way we live, the developing world is where their vision is revealing itself most clearly. In Kenya, for example, the payment messaging service M-Pesa has attracted over 13 million monthly active users (out of a population of 44.3 million). As of last May, roughly 42% of Kenya’s GDP was transacted via M-Pesa, all without tying Kenyans to expensive, cumbersome bank accounts.

But more than that, M-Pesa has effectively invented a new form of credit that’s based on a history of reliable transactions from phone to phone, rather than through a bank. In a world where 2.5 billion people don’t have bank accounts, systems like M-Pesa are set to leapfrog Western banking the same way much of the developing world skipped the desktop and went straight to the smartphone for its computing needs. In reinventing money transfers, M-Pesa and its ilk offer more than a new way to pay — they are opportunity engines, offering the ability to build credit in a world that previously shut them out. And in the process, there are billions to be made in transfer fees.

By my third week, the cashless, frictionless future I’d hoped to live began to feel glitchy, burdensome, and alienating. I had to meticulously plan my every move hours or even days in advance — a haircut required me to convince my barber to start using Venmo, going out for a meal meant lining up a dining companion willing to submit to confused stares and drawn-out check-settling processes.

One January afternoon, I found myself trying to persuade a prodigiously bearded, flannel-shirt-wearing barista named Michael to allow me to pay him personally via Square Cash for a coffee, which he would then pay the register for. After a confession that this was all for a story from me and a pity laugh from him, Michael reached for his phone, but not before he locked eyes with me. “I’m only doing this because I want you to write about how much this sucks for us,” he said. He went on to talk about a popular coffee app called Cups, which allows customers to order and pay all inside the phone. “It’s like, now everyone who comes in is a robot — they just stare at their phone and wait to have their name called. Nobody even looks at us,” he said.

At this point, replacing my wallet with a phone struck me as little more than a shallow gimmick, an academic exercise, like living in a house mid-construction, before the appliances work and the water and electricity have been switched on: It’s entirely doable, and chances are no one’s going to get hurt, but that’s an awful reason to do anything. I needed something more drastic, which is how I found Hannes Sjoblad, who told me, with surprisingly little fanfare, that he could make me a cyborg.

When I contacted Sjoblad, whose LinkedIn profile lists him as the chief disruption officer at the Swedish biohacking group BioNyfiken, he’d been experimenting with NFC and RFID chip implants by hosting chipping parties for curious biohackers-to-be. His xNT NFC chip is really just a prototype: Sjoblad’s implantees are guinea pigs testing out what they believe could become common uses for a technology that’s usually reserved for phones and credit cards. Sjoblad himself uses his as a replacement for his house keys, business cards, and bike locks.

I asked him if I could use the chip — the same kind, more or less, that sits in and powers the Apple, Google, and Samsung Pay parts of our phones — to pay for things in a store; he wasn’t sure, but he knew a programmer who could link it to a bitcoin wallet. We Skyped once and formalized plans to make me an implantee. “I think when you meet us you'll see that we're pretty normal mainstream persons,” he told me over a grainy video chat. “We're not like some underground den of hackers.” He let out the kind of nervous, mischievous laugh you might let slip if you ran an underground den of hackers.

In the meantime, if I couldn’t bring the future to myself, I would have to do the next best thing: get into bitcoin. At its most basic, bitcoin is the very complicated product of advanced mathematics and cryptography, a “peer-to-peer system for online payments that does not require a trusted central authority.” Bitcoin can be mined by those who donate part of their computing power to help verify the peer-to-peer transactions going on in bitcoin’s ecosystem via the blockchain, which is a string of bundled past transactions. (It's a bit like if you loaned part of your computer to your bank to help it process payments across the world and got a very tiny reward for the donation). But bitcoin's real beauty, according to its disciples, is that it’s not really governed by any entity, making it nonreversible, unfreezable, and anonymous, all with very low transaction fees. It's a powerful idea, and bitcoin has been a bolded and underlined bullet point in every future-of-finance argument. But in 2016, almost eight years since its creation, using bitcoin is a world-class exercise in frustration.

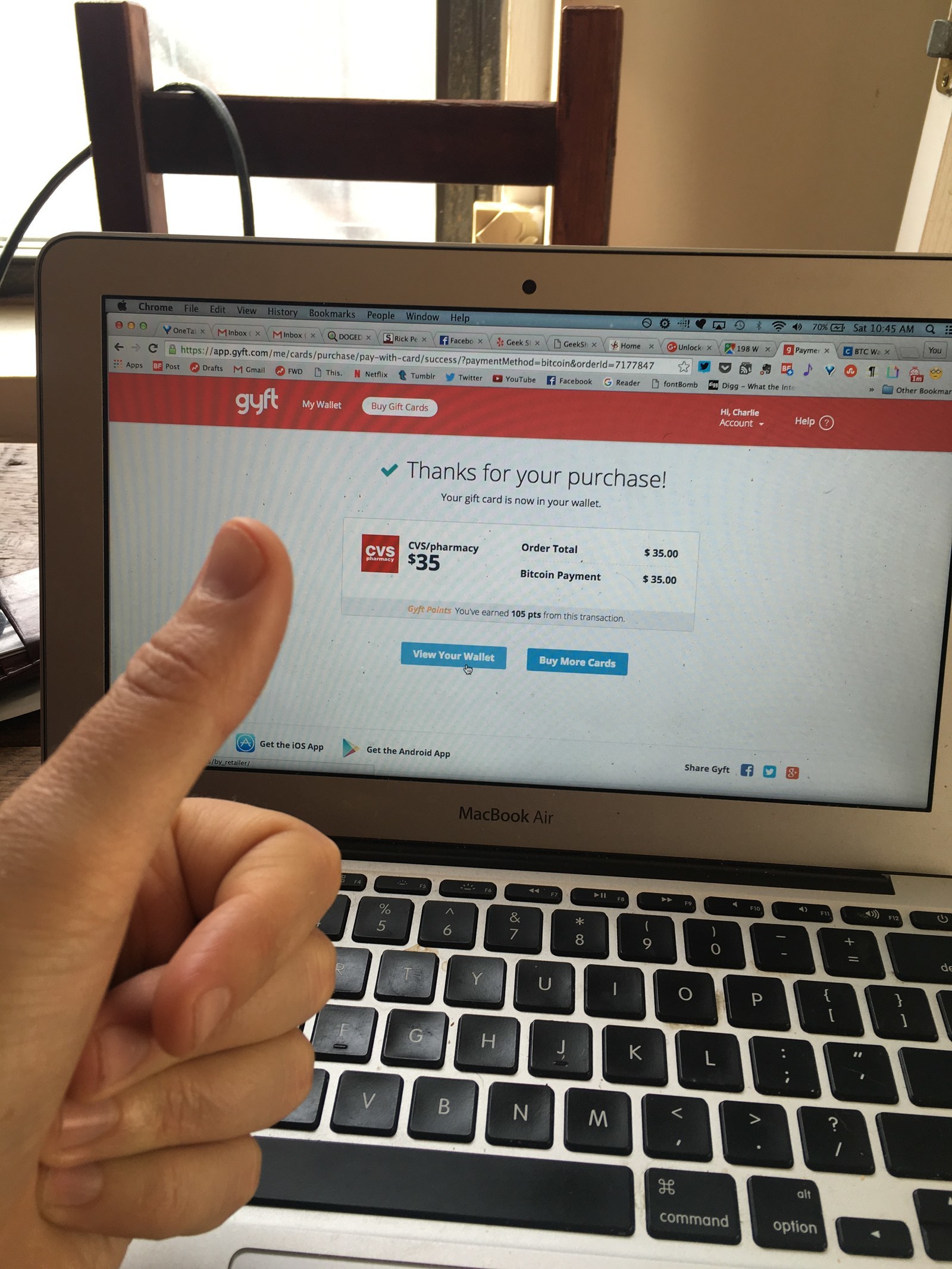

If living without cards and cash meant planning all my purchases in painful detail, living without state-backed currency of any kind only exacerbated the problem. To buy anything immediately out in the physical world, I had to use bitcoin to buy gift cards and then redeem them at the store for groceries, meals, and anything else. When I ran out of toilet paper, I loaded up Gyft, a digital gift card site, and purchased a $15 CVS card, which I then redeemed for Cottonelle as the store opened — all told, a 45-minute ordeal. Splitting the bill was impossible without a friend willing to set up their own bitcoin wallet, and sending money through bitcoin's blockchain technology felt almost purposefully intimidating, with long, wonky wallet addresses, exchanges, and codes.

And again, there’s trust — using bitcoin means transferring real money into a volatile currency, which hit home when bitcoin’s value dropped almost 18% just hours after I converted $800 dollars to book a flight. Though today bitcoin is niche but somewhat stable, it’s not exactly hard to imagine the whole thing melting down overnight. (As a challenge, my editor tasked me with buying something “tangible” with bitcoin’s jokey, basically defunct cousin, Dogecoin: I was rejected by a meme memorabilia merchant on Etsy when I asked to pay for a mug with a cartoon frog using Dogecoin. A new low.)

But simply replacing paper dollars with digital ones isn’t the draw for bitcoin’s biggest advocates. Olaf Carlson-Wee, a 23-year-old early employee at the bitcoin startup Coinbase, has been living almost exclusively on bitcoin for three years. "The exciting things are not where bitcoin competes with regular money," he told me, "but where the tech is so radically different it creates new modes of behavior.” Carlson-Wee sees apps like Apple Pay as “abstraction layers,” basically just a digital copy of a common credit card — unlike bitcoin, which is a whole new platform.

Adi Chikara, a strategist for 3Pillar Global who has been advising on and investing in companies using blockchain technology for years, sees its elegant, unbreakable cryptographic security as a new way to ensure trust. In some scenarios, he argues, blockchain technology can act as a replacement for currency as a whole. Imagine a system where legal contracts are automatically executed through the blockchain — for example, your monthly car payments are directly linked to your ability to unlock your vehicle and put it in gear. The particulars are complicated, but blockchain has the potential to act as a powerful reinvention of 21st-century bartering. It’s also, ultimately, maybe the only way to ever move past a state-backed currency.

"It’s solutioneering: Take something that exists just fine and make it digital and somehow we’re all supposed to believe it’s better.”

“We had paper and it was backed by gold, and right now we're trusting the government — but with the blockchain you may not necessarily need the state,” Chikara told me. The early signs of this are around today — Circle, for example, is a peer-to-peer money transfer app, similar to Venmo, which is powered by the blockchain, meaning, unlike Venmo, the payments are instantaneous and can easily be converted into different currencies without fees.

Chikara readily admits we’re years, if not decades, away from a viable, universal blockchain-centric financial system. Like Venmo and Apple Pay and cash, bitcoin is still subject to human error, like in 2014, when the executive in charge of Mt. Gox, a popular cryptocurrency exchange, embezzled and lost hundreds of millions of dollars worth of bitcoin. But Chikara still proposes a scenario with no banks and no federal reserve.“There is no printing of money,” he said. “It's owned jointly by the people themselves, and they trust each other.” Blockchain technology is already being tested by traders across the world and has been implemented in the Australian stock exchange. IBM, Nasdaq OMX, Intel, and Cisco are exploring the blockchain and blockchain-based open ledger projects for trading, along with banks like Wells Fargo and JPMorgan. And recently Goldman Sachs filed a patent for SETLCoin, the company’s very own blockchain-powered currency.

But perhaps the best description of bitcoin’s potential came from Coinbase co-founder Fred Ehrsam, who sees blockchain technology as nothing less than the most significant open platform since the web. “We take what was once a highly controlled system and turn it into a software development problem where people can go nuts,” he said. “And it becomes like the internet, where you have a big open network, people can build whatever they want. The market decides what's good and what's not. And before you know it, you have this great big open network that has all these great ideas on it and things can really start to get interesting.”

It was the beginning of week four and bitcoin had driven me deeper into my hermetic state — most of my purchases were being made online and my relation to the real world was almost exclusively conducted through a screen of some sort. I needed a change of scenery.

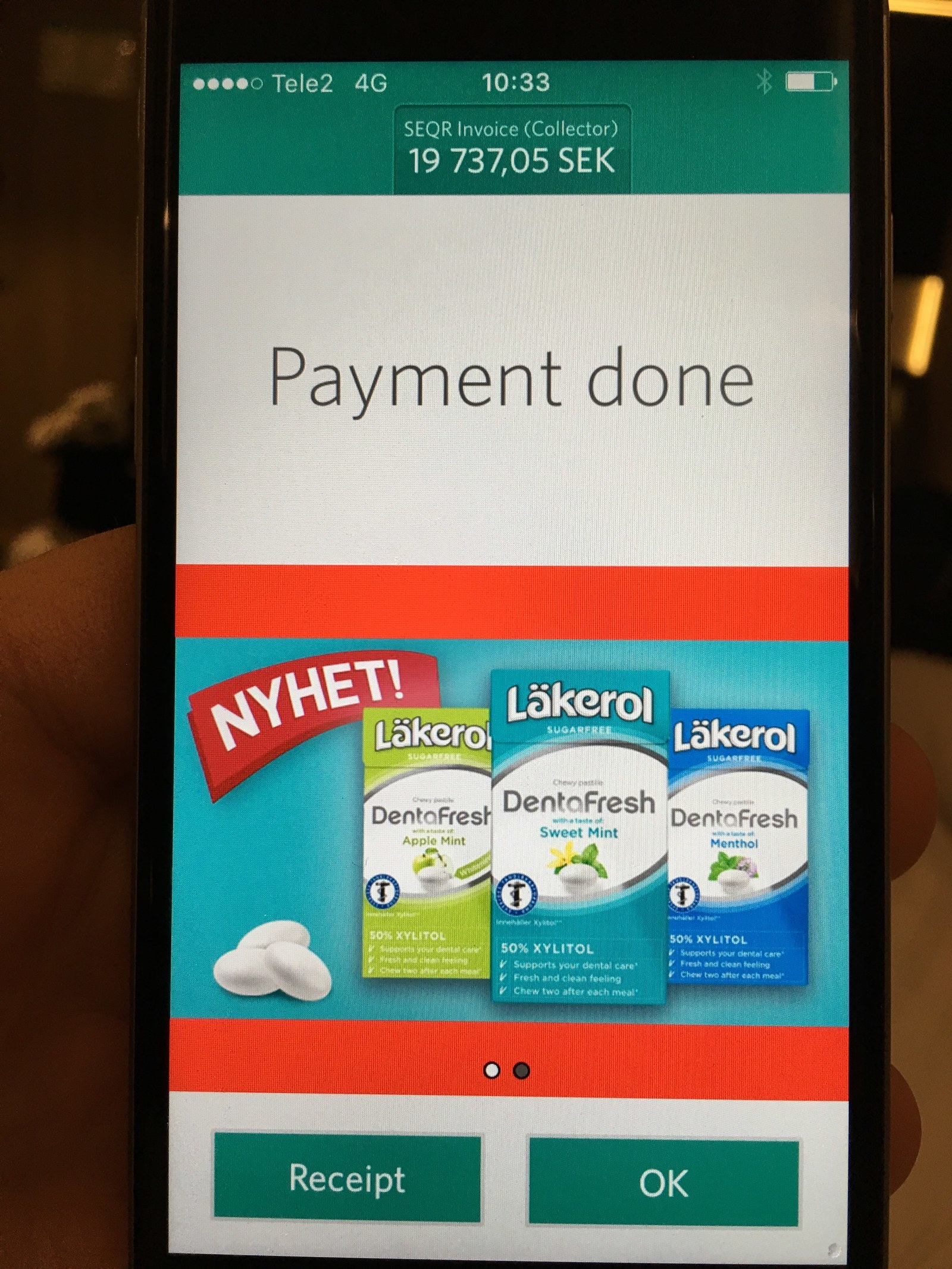

As it turns out, if you yammer about the future of money long enough, somebody is likely to tell you to go to Sweden and see it for yourself. There, among the bountiful sweaters, sunless winters, and impossibly good genes, is the closest thing you’ll find to a truly cashless society. Just 20% of all consumer payments are conducted using cash in Sweden; according to a 2015 survey, only 2% of Sweden’s economy revolves around the ancient, dirty exchange of paper money and coins. I booked my flight rather painlessly using bitcoin (thanks, Expedia!) to figure out how and why 9 million polite socialists have beaten the rest of us to the paperless money future.

With its standing desks, glass-walled meeting rooms, and long corridors lined with stark black-and-white portraits, the office of Situation Stockholm looks like a startup. In fact, it’s almost the complete opposite: a 21-year-old glossy print magazine sold primarily by the city’s homeless population. The portraits on the wall are of the magazine’s vendors, who are, incidentally, some of the first pioneers of cashless street busking.

“A common response from presumptive customers was 'Sorry, I don't have any cash,'” Jenny Lindroth, an operations manager at the magazine, told me. “So we started to think of ways to take this cash business — a lot of our vendors don't have bank accounts — digital.” In 2007, Situation Stockholm started giving select vendors the ability to sell the magazine by having customers text a number, which would then add a charge to their cell phone bill. In 2013, the company bought card readers from a Swedish payment company called iZettle and sent its most reliable vendors out with them.

Since then, Situation Stockholm has seen an uptick in sales for vendors, as well as a newfound agency. “People outside the country seem to think that it’s interesting or funny that homeless people have these phones and card readers, but it's not really big news here in Sweden,” Lindroth said. “It's just common practice now — in Sweden you don't have cash.”

Walking around Stockholm’s icy cobblestoned sidewalks and winding, low-arched alleyways, I found myself ducking into countless shops, bars, and konditori cafés, eavesdropping on checkout registers and craning my neck for a peek at local wallets. Not once did I see a paper bill. Paying by phone was commonplace, and I didn’t even get a weird look when I scanned a QR code at a grocery store checkout and wordlessly strolled away with my basket of smoked meats.

According to Jacob de Geer, the CEO of iZettle, Sweden’s cashlessness can be traced back to the early 1990s, when tax subsidies encouraged citizens to buy early personal computers en masse, thereby making the country extra technologically adventurous. But all that early adoption hasn’t been easy for everyone. Swedish banks have drastically cut back on ATMs, raised cash transaction fees roughly 300% in the last four years, and made depositing as inconvenient as possible. Recently, Lindroth witnessed an elderly woman being turned away at the bank after she attempted to deposit a large amount of cash she’d been storing at home. “If she had transferred that money from her phone, she wouldn’t have been questioned in the same way.”

The problem, according to Björn Eriksson — a former head of the Swedish police and Interpol, and a prominent dissenting voice in the country’s rush to cashlessness — is not the end of paper money, but the speed of the transition, which is especially hard on older generations, those in rural areas, tourists, and new immigrants who come to the country without cards or bank accounts. “It’s gotten so that some people are resorting to hiding money in their microwave because they have nowhere to put it,” Eriksson told me. It can even be dangerous to public health: Just last September, Sweden’s highest court ruled against the Kronoberg County Health Authority and reprimanded them for not accepting cash as legal tender for medical services in all but two of their health clinics.

Access to new technology is never evenly distributed. And even those like iZettle’s de Geer, who are enabling and profiting from a digital payments revolution, have reservations about abandoning paper money outright: “Everyone thinks I'd like to see the death of cash, but privacy is a big issue for all of us. Cash’s benefit is privacy. There's plenty that's legal to buy out there that you don't want everyone to know you've bought.” If America is headed down Sweden’s cashless path, we have much to learn from our Scandinavian friends. Or get comfortable finding stacks of twenties in the fridge next time you're at grandma’s place.

As I pushed through the door of Calm Body Modification, a bell tinkled amiably, as if to reaffirm the shop’s namesake. I looked up at the proprietors, tall men with all their exposed skin covered in tattoos. Above one, a sign advertised genital piercings for 1,000 kronor.

My piercer, Chai, and I retired to the backroom where my skewering would take place. “So now I’m going to tell you something you probably didn’t consider before,” he said, furrowing his brow. “People — very conservative right-wing Christian types — might come after you for this. They see it as the Mark of the Beast. I just want you to be prepared.” I nodded like this is something I had expected to hear.

This comes from the Book of Revelation: “And he causeth all, both small and great, rich and poor, free and bond to receive a mark on their right hand, or on their foreheads; and that no man might buy or sell, save he that had the mark, or the name of the beast or the number of his name.”

The passage essentially describes a closed economic system, where power is consolidated and financial gatekeepers can shut anyone out. It made for a potent metaphor. I’d spent the last three weeks in search of a connected, seamless future, but I found myself more separated than ever from the people around me.

Around week two, I’d noticed how robotic my interactions had become during any financial transaction: walk into some reliable big-box establishment, mumble order, flash phone, move down the line. Moments like my conversation at the coffee shop with Michael, the barista, heightened these concerns. The brick-and-mortar world of commerce is in the midst of a rewiring — one that’s supposed to bring in more merchants and give consumers more access to what they want when they want it. But that means new behaviors, some of which are likely to be harmful.

New commerce apps and technology may have a lower barrier to entry than, say, credit cards, but many of these programs — like miles cards — reward you and work best when you’ve got money to spend. And while much of fintech is billed as liberating us from the old ways and institutions, new gatekeepers are bound to emerge, in many respects, guiding us — perhaps unwittingly, at times — toward the outcomes that their data analysis has told them we want.

Bitcoin evangelists are optimistic, but the legacy banking system is as inescapable as it is flawed. Even today’s most disruptive money solutions are still reliant on traditional institutions. While Kenya’s M-Pesa allows money to be transferred from phone to phone outside of banks using the cellular company Vodafone’s network, at the end of the day, the transferred money is still backed by the pooled accounts held in regulated commercial banks.

Bitcoin or blockchain-based currencies could free us from the tyranny of service fees and interest rates and all the regulations that complicate and ultimately exclude merchants and large populations from the global economy. Or bitcoin could be adopted by legacy institutions that will strip the technology of its open platforms and use it to create a slick, more efficient model of the current system.

The fumes from Chai’s alcohol swab jolted me back into the moment. “OK, just a slight pinch, here,” he said. “Sometimes it helps to look away.”

Being chipped was oddly anticlimactic. A trip to the doctor revealed that I hadn’t done anything too horrible to myself. “Wait, you’re telling me I can unlock doors with that thing?” my physician cheerily inquired when I asked if I should be worried about my body rejecting the chip. “I might have to get one myself!” Over the course of a few weeks, the whole thing became an afterthought; a piece of me that stored information, like a low-tech flash drive that I couldn’t misplace.

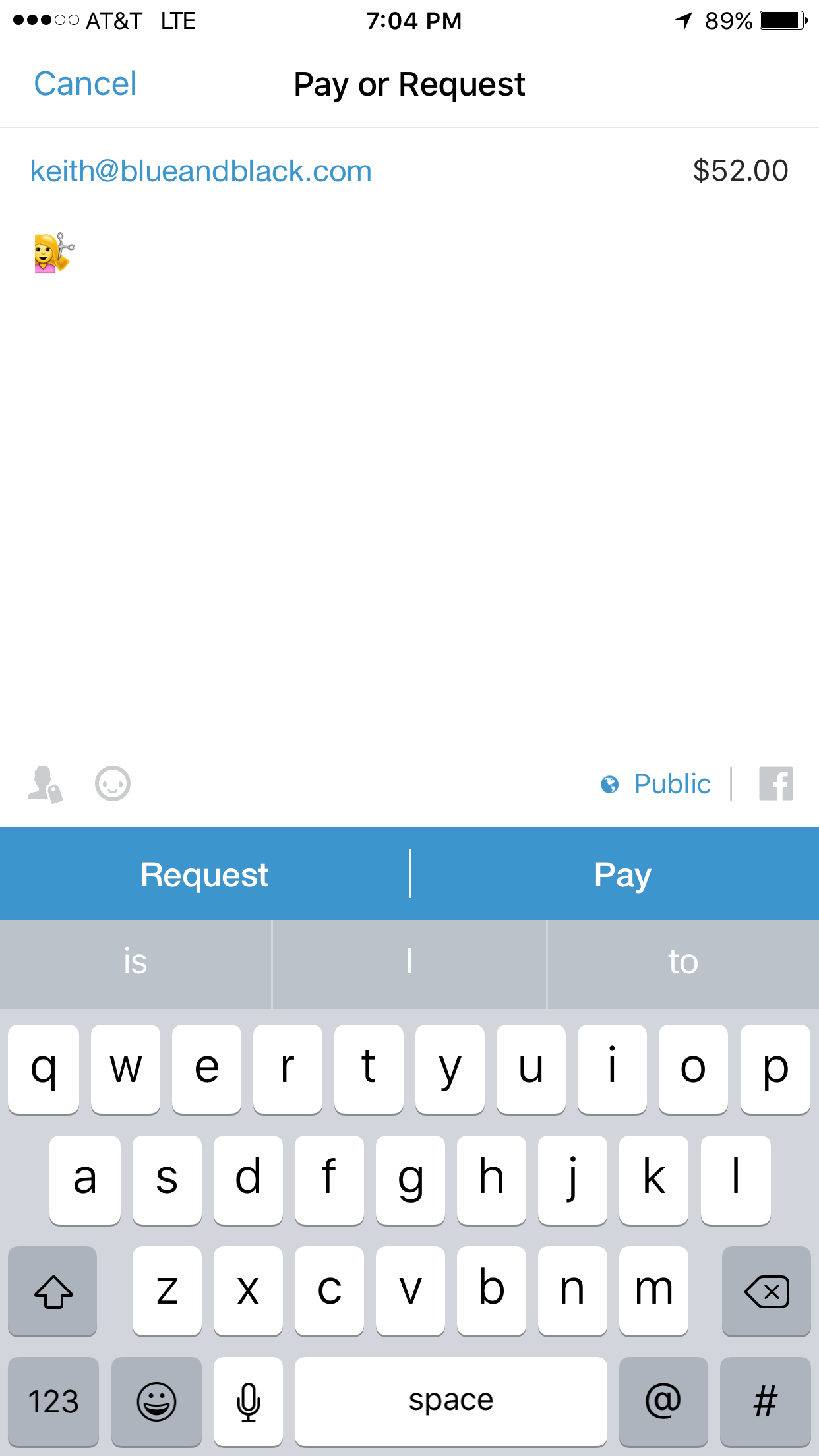

But there was still the problem of payments. I reached out to former Venmo employee and co-founder Iqram Magdon-Ismail, who then enlisted the help of Nuseir Yassin, another former Venmo employee, to help me become the first person to pay for a meal with his hand.

I asked Magdon-Ismail, who’d had a hand in building one of the most successful person-to-person money transferring apps, to explain the allure of the payments industry. “One side effect of this industry is that you make a lot of money if you move a lot of money," he said. "If you're serving an underbanked community with a financial product, you get a couple hundred thousand users and you make a small return on each one of them — well, that's a really good business, right there.”

“It's a big pie,” eMarketer’s Yeager said of the money to be made in the payments space. “It's going to be around $100 billion by the end of this year, and that’s just retail mobile commerce.” Similarly, Jeremy Allaire, who runs Circle, cited a study by the Aite research group suggesting that personal payments in the U.S. is a $1.2 trillion market, 90% of which is cash and checks. “What if you can help introduce a new behavior?” he said of the opportunity to capture some of that money.

As Alex Rampell, a general partner and fintech investor at the Silicon Valley venture capital firm Andreessen Horowitz, told me, the genius of Apple Pay isn’t in the "tap to pay in the physical world" at Whole Foods but the ability to store payment credentials and personal information for millions of cardholders and create a one-touch fingerprint payment method across the entire web. If successful, Apple will have cemented itself as the most widely used and reliable online payment passport, allowing consumers to stop paying premiums at online retail giants like Amazon for the simple convenience of one-click payments. And then, Rampell suspects, Apple will make the digital wallet available to developers.

I’d spent the last three weeks in search of a connected, seamless future, but I found myself more separated than ever from the people around me.

“If Apple and Google are smart about this, they’ll encourage opening the wallet up as the next platform,” he said. “Imagine allowing budgeting apps like Mint to operate on top of the wallet so that they help you budget your finances in real time. Or allowing lending companies to build a plugin to the Apple Wallet so every person who uses Apple Pay saves 50% on their interest rates? That could force a company like Capital One into bankruptcy by no fault of its own. And that’s a big, big deal.”

All that potential is intoxicating. Over the course of my month, I found myself unexpectedly buying into the possibilities of bitcoin, seduced by the ease of phone-waving payment. It feels good to be hopeful about these things, to imagine that there's a way beyond crazy fees you never asked for — a way to replicate the safety, trust, and stability of banks without their consolidation of power and bureaucracy. But disrupting at software speeds in the physical world means feeling growing pains — usually important, ignore-at-your-own-peril signals — without having time to consider and interpret them. It turns progressive early adopters like those in Sweden into a system that can exclude its elderly and consolidate power in a handful of banks, all in the name of some kind of progress. The future of money is coming — there’s no stopping it. But there is a matter of control, of receiving the future incrementally and responsibly.

Weeks passed and normal life returned, save for the still-unused microchip in my left hand. It had become a life raft for the experiment, which had largely failed to yield the kinds of aha moments I had assumed I'd be having when I locked away my wallet. And despite the hype and the influx of money and the feeling that everything is just about to change, it’s going to take real time. (It’s very much worth noting that just in the week before this story was published, the fintech peer-to-peer lending darling Lending Club’s CEO resigned over an internal probe concerning improper loan sales; a security breach in a Hong Kong cryptocurrency exchange resulted in the loss of at least $2.14 million; and the massive retailer-led consortium MCX has significantly delayed — perhaps killed — the rollout of its digital wallet, CurrentC, to “concentrate more heavily” on other non-mobile-commerce areas of the financial sector.) That’s because today's fintech is more evolutionary than it is revolutionary. And when this change does happen, it will do so on the backs of a new generation that isn't just asking for a new money model but is demanding it. Buying a sandwich with my fist isn't some paradigm shift — it's a stand-in for something weightier: a future that feels just a bit less recognizable.

One April morning, my inbox pinged. I’d given Yassin full access to my Venmo account, after which he set up a server linked to my unique Venmo payment key. Now his code was working in test runs. We picked a restaurant — a Sri Lankan place on New York’s Lower East Side that’s partly owned by Magdon-Ismail and of course accepts Venmo — and Yassin coded the chip so that it would launch a website on the merchant’s device when scanned. The site would trigger a payment from my Venmo account with an automatic 20% tip. All I’d need was my hand.

We got to the restaurant a bit after noon on a cold, rainy Monday. Absentmindedly forking spicy lamb into my mouth, I was sure we’d be derailed by a glitch or a bug. Word of the impending hand payment spread in the cramped restaurant. Our waiter, a friendly guy in a flat-brimmed Yankees cap and a Teenage Mutant Ninja Turtles T-shirt, was excited but announced his skepticism. “This is crazy, dude,” he said, half excitedly, half exasperatedly.

When the bill came, I ambled up to the counter of the cramped restaurant as the other diners craned their necks. Our waiter held out the phone as I thrust my clammy fist forward. Nothing registered. My stomach dropped. He waved the phone like a metal detector around the whole of my fist. Finally, a beep. We locked eyes, pupils dilated. Numbers were input. Another beep. Then, the ching of a cash register. The sweetest sound. •