"What people want is not to fuck it up," said Jon Stein, the 34-year-old founder and chief executive officer of Betterment, a software-based financial advice company.

Stein is referring to the massive skepticism people have — particularly the twentysomething cohort collectively referred to as "millennials" — about investing in the stock market, which is driven by the sting of witnessing their first financial crisis five years ago and the lack of faith in traditional financial advisers it engendered. Young people, who according to standard investment advice should be taking more risk by investing in stocks and having greater long-run returns, are instead holding more money in cash. This means that a large number of them have been sitting out a sustained run up in asset values. The S&P 500, for instance, returned 32% in 2013 and 91% since 2010.

"The crisis merely confirmed the doubts that young people already had of Wall Street and financial services firms," Merrill Lynch's director of behavioral finance, Michael Liersch, wrote in a report. Added Chris Lucy, the managing director of Accenture's wealth and asset management services group: "[Young people] are less likely to take at face value the credential that a wealth manager might have brought to a prior generation."

Betterment, Wealthfront, and a number of other automated, or software-based financial advising startups, have formed their business models around this generational disconnect. (Betterment has raised $45 million, while Wealthfront has raised $65.5 million.) Their bet is that young people aren't disenchanted with the idea of investing, just with the traditional stock market gatekeepers.

Bay Area-based Wealthfront, run by former LinkedIn executive Adam Nash, is the largest of this new breed of companies, with $1.1 billion under management. Betterment, founded by Stein and Eli Broverman, has amassed $625 million in client money since 2010. The average age of clients is 36 at Betterment and 35 at Wealthfront, and they skew heavily (though, they would insist, not exclusively) from the technology world. Their basic pitch is simple: Trust that academics have it right about how to best invest and trust in software to best execute that strategy.

"Software doesn't sleep, software doesn't take a vacation, software doesn't tell one customer one thing and tell another customer something else. Software doesn't have a vested interest in promoting a certain stock," said Stein.

The firms, which have several startup competitors along with brokerage behemoths like Fidelity and Charles Schwab, have slightly different investment plans and features but are based on the idea that the overwhelming majority of people with enough assets to think about investing are best-served by low-cost investments that track indexes and are automatically rebalanced over time.

Young people are much more financially conservative than other investors.

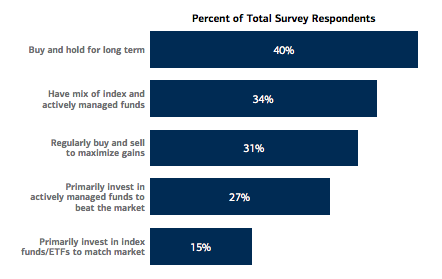

Indeed, there's been a wave of newfound interest in investing in index funds and broad-market ETFs, mutuals funds and stock-like funds that try to track a broad index like the S&P 500. Nearly 20% of all stock mutual fund assets are currently controlled by index funds, compared with 9.5% in 2000. Actively managed domestic stock mutual funds have seen net outflows of $575 billion in the last five years, according to the Investment Company Institute, while in 2013, $114 billion flowed into index funds. There was similar growth in index ETFs — some $99 billion of shares in broad-based stock ETFs were issued in 2013 compared to $58 billion in 2012.

What these automated financial advisers offer is a way of realizing the widely held academic view that individuals are very unlikely to outperform simple investing benchmarks over a long period of time and that a low-cost portfolio of stocks and bonds (and in the case of Wealthfront some other assets) can provide satisfactory risk-adjusted returns.

Wealthfront's chief investment officer, the economist Burton Malkiel, is the author the best-selling A Random Walk Down Wall Street, which critiques methods of analyzing individual stocks and argues that the best risk-adjusted strategy is to have a diverse portfolio of investments that changes as you get older. Betterment's stock ETFs are slightly tilted toward small-cap and "value" (i.e., cheap relative to its fundamentals) stocks, based on academic work done by Eugene Fama, who also first formulated the efficient markets hypothesis.

"If you expect the world economy will grow, then asset values will grow," Stein said. "The two should correlate over time, and historically asset values have grown faster than the world economy."

Even wealthy young people favor conservative investing strategies.

A survey conducted by UBS, the Swiss bank that manages $158 billion of client money in the U.S. alone, found that people between 21 and 36, with two recessions fresh in their memories, are remarkably conservative financially. Seventy percent of people in that demographic in the UBS survey described their risk tolerance as moderate, conservative, or somewhat conservative. The survey also said that young people "now define risk as permanent portfolio losses" (as opposed to transitory losses or missing out on potential gains), and this is reflected in very conservative decisions about saving and investing that run "directly counter to traditional long-term investment allocation advice."

it's not just young people in the U.S. who are shifting away from stocks — globally, stocks have gone from 51.6% of the overall market portfolio in 1990 to only 36.3% in 2012, according to a paper published in the Financial Analysts Journal.

"This generation now that we're claiming is underinvested, when they hear 'stock market,' they only think risk," said Josh Brown, the CEO of Ritholz Wealth Management. "Their formative experience is seeing the S&P 500 cut in half twice in the past 15 years, you'd have to go back to the 1930s to see that much pain was compressed in that much time."

Only 28% of young people said that "long-term investing" was one of the three most important factors in achieving success, according to the UBS survey, compared with 52% of the rest of the population. And just 12% of millennials would "invest immediately in the markets" if they were given additional money, compared with 33% of the rest of the population.

"Millennials overwhelmingly want to focus on their passion — work, family, friends, hobbies," said Wealthfront's Nash. "What they don't want to focus on is managing money. They don't believe their path to success is taking money and turning it into more money."

While Wealthfront and Betterment have new offerings to cater to their customer base — the former, for instance, has a tool for managing the sale of a large employer-stock position slowly — they'll never offer the highly personalized service that financial advisers roll out for their richest clients (think golf games, exotic car financings, loans backed by contemporary art). For Betterment's Stein, losing out on the ultra-high net worth market is fine since, as he claims, "we're the best solution for anyone with $10,000 to $10 million."

The drawback, however, is that focusing on lower account balances means that the firms are leaning on software's unique ability to scale to service huge numbers of clients. Betterment charges 0.15% for customer balances greater than $100,000 and 0.35% for balances $10,000 and below, while Wealthfront is free for the first $10,000, and then charges 0.25%. Independent fee-based asset managers tend to charge more than 1%, while a Charles Schwab ETF portfolio will cost between 0.9% and 0.5% depending on the size of the account.

The low fees mean that the software advisers have to get a huge number of clients to achieve the profitability that their investors expect.

"We can't take credit for the revolution for passive investing and index funding," Nash said. "What you see in any industry is that when you have a revolution, you then ask what you can build on top of it."